The Impact of IoT on FinTech & Banking

4 June 2020

2

2

2

2

5k

5k

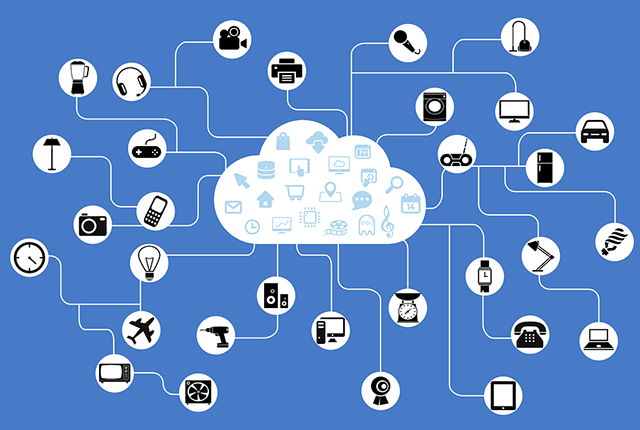

In an increasingly connected world that is increasingly

dependent on technology and all its benefits, one innovative area of digital is

contributing to its mass adoption worldwide; the Internet of Things. IoT

basically pertains to common things in our daily lives that are now connected

and online. Wearables are seeing more commercial appeal and popularity, and

everyday appliances and objects around our homes are connected more and more, enabling

‘smarter’ homes and easier lives. According to Business Insider, 64 billion IoT

devices are estimated to exist by 2025, an impressive difference when compared

to 10 billion in 2018. McKinsey also states that 127 new tools are connected to

the Internet every second.

Where FinTech is concerned, the most affected areas with

IoT-related changes are customer service, security/safety, repayments, internal

procedures, and facilities. IoT can provide a unique edge to financial

institutions through several touchpoints, and offers many benefits in banking

& FinTech.

FinTech as an industry has been deploying AI-powered

solutions for some time now, albeit not without human assistance in most cases.

Collaborations with banks and traditional FIs enable them to provide instant

access to FAQs and general support for customers, and this direction is further

empowered by IoT devices, as smart gadgets act as a platform to leverage IoT

technology for enhanced efficiency and quicker serving times, raising overall customer

satisfaction. A personalized experience and customized care are crucial to

establishing loyalty & trust, and are achievable by using context-aware

smart solutions.

IoT and FinTech can be utilized in all sorts of ways inside

physical bank branches or any other financial institution. From queueing apps

that enable virtual lines to save time & effort to instant messaging

services with suitable agents that provide quick solutions on the spot, a visit

to your bank is becoming much easier and less time-consuming. A basic example

of using IoT technology in branches is to perform electronic ticketing, where a

customized solution and destination inside the branch are given to customers

based on their specific need. It’s also logical to assume that, as these

services evolve, the need to make actual physical visits to local banks will

diminish and people will be able to do most of their banking operations online.

Should they need to go to the bank, technology will also be there to help them

reach their goal faster and more efficiently.

Electronic payments are slowly but surely

becoming the preferred method of payment for most people with access to FinTech

services, due to their speed, reliability and ease of use. Today, wearables

like smart watches and smart wallets are replacing smartphones and physical

credit cards in digital payments and even cash withdrawals. Reaching over 1.1

billion devices and up from 526 million in 2016 in an estimate by Statista,

it’s obvious that wearables today are in fashion and are here to stay, as

people are adopting their convenience and safety around the world.

IoT gadgets are being used today as verification

methods in FinTech, as biometric authentication can make use of a person’s

heart rate to identify them. What can be more reliable than that! This

reinforces safety and security of banking through IoT devices, one of the

primary concerns of customers when it comes to using FinTech applications. Another

aspect of FinTech where wearables come in handy is self-checkout services. People

today can swipe their smartwatch or smart wristband at cashiers in certain stores

to pay for their groceries and just walk out the door.

The uses of IoT devices are plenty and as FIs

continue evolving their digital strategies, IoT is participating more and more

in those strategies. The general direction is that they will eventually take

over mobile phones for payments and secure transfers, seeing as their

convenience makes that much easier. IoT-enabled security systems are finding

their way to consumers and they create a personalized access experience and

reliable identification method for their owners. People are able to sign, pay

and pretty much do everything that a smartphone offers using their wearables. This

also provides many advantages to financial institutions, as they have an open

channel with their customers and can relay all sorts of customized messages and

financial updates about their accounts. Users in turn can get to see they

transaction history and expenses on their wrists and around their necks on the

go.

It seems that the Internet of Things is an area of technology that will elevate the personalized aspect of FinTech to a whole new level. As banks continue to restructure their strategies and adopt innovative concepts and technologies, it would be smart to consider potential solutions using access to IoT devices to stay relevant and competitive in the digital finance market. Functionalities of smartphones are quickly being integrated in wearables and IoT devices, which entails that most operations currently done through mobile phones will eventually be available on smartwatches and wristbands. IoT is still a relatively new domain, and relevant expertise in developing its solutions is scarce when compared to other areas, however it is the great degree of customization and personalized experiences that could ultimately prove to be the most important factor to customers, and so FIs should prepare to deploy their solutions on those innovative platforms in the coming period.

related articles

Mutually Beneficial Partnership Scenarios for Banks and FinTech Companies

How FinTech is Revamping the Insurance Sector

Financial Health is What FinTech Should Be Empowering

How IoT is Infiltrating FinTech Payments

Can the Middle East Bloom Into A Global FinTech Hub?

Setting Digital Banking Transformation Priorities During a Pandemic

The Challenges that FinTech Startups in Emerging Markets need to consider

Four FinTech Elements Affecting the Retail Banking Ecosystem

The State of Biometrics in 2020 and Beyond

Regulatory Technology is the Unsung Hero of Digital Transformation

Bridging the Digital Divide with APIs

Shifting from Disruption to Innovation through FinTech Partnerships in COVID19 pandemic.

Going Cashless is the new way to go in a Post-Coronavirus Future

Relevance of Scheduling Apps for Bank Appointments is Skyrocketing

How is Banking Changing with COVID-19?

Customer Service Transformation has become a must in a Digital World

The Opportunities and Threats of FinTech during COVID-19

How FinTech can relate to the Healthcare Industry

The Impact of Coronavirus on the Financial Sector

FinTech’s Critical Role in the Battle Against the Coronavirus

6 Benefits of Blockchain Technology in Finance

Humanizing Services through Smart Banking Technologies

MSME Lending & FinTech: What to Expect in 2020

How Digital Innovation can Transform the Future of Banks

Banking Experts Forecast Key FinTech Trends in 2020

How FinTech is Changing the Finance Industry.

6 FinTech Trends That Will Transform Banking In 2020

FinTech Trends To Keep An Eye On In 2020

How FinTech Can Contribute To Healthcare

How many digital Middle Eastern companies have unlocked their full innovative potential?

Singapore FinTech Festival 2019: A Meeting of the Minds

Digital Banking vs Physical Branches: Competition Not Mandatory

BEBA presents the Digital Assets & Artificial Intelligence: Shaping the Future event

UAE-based FinTech startup Foloosi raises $500,00 in seed funding

Five Technologies Expected to Reshape FinTech in 2020

.jpg)

Is Authentication by Facial Recognition an Ideal Method to Combat Financial Fraud?

.jpg)

Egypt’s First Artificial Intelligence Faculty launched at Kafr El Sheikh University

Comments

Awesome

10:51:38 AM 14 July 2020nice!

10:51:50 AM 14 July 2020