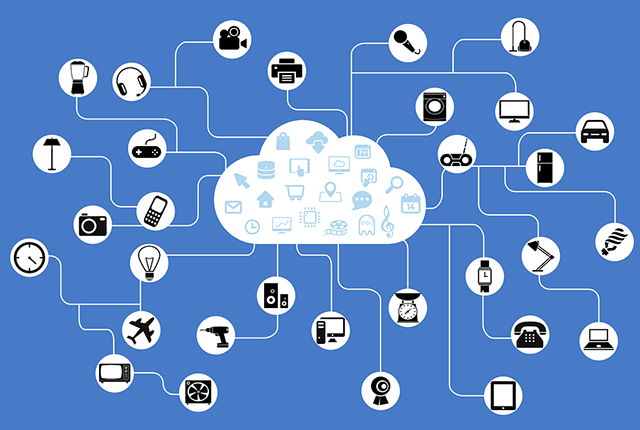

Using everyday things to make payments might have been farfetched at some point in the digital age, but today the Internet of Things or IoT is a very real concept that is increasingly making its way into the digital finance industry, and consumers are slowly adapting to the fact that they can now communicate with household items to simplify all related financial aspects.

IoT as a concept has been around for some time but hasn’t really seen traction until recently, and now with the rise of technology adoption rates due to the ongoing impact of the Coronavirus pandemic, the world is seeing more commercial IoT applications, and the Fintech industry is no exception.

In line with the traditional finance industry’s skepticism on digital finance, IoT was dismissed at an early stage as just another digital buzzword that wasn’t projected to have any real impact on the finance world. However at this point, IoT is already embedded in our daily lives through e-commerce platforms, and the world is already using billions of IoT devices without necessarily knowing it.

So let’s discover how IoT is currently integrated into FinTech and subsequently, our lives.

E-Wallets have been available for a while from different banks and financial institutions, and the term wallet hardly pertains anymore to the physical holder of cash and personal items. Many e-wallets create expense patterns and understand user behavior to project their expenditures and manage their budgets seamlessly IoT devices.

A common presence of IoT in FinTech is found in smart security systems that are concerned with access control, and identification protocols used in banks and other financial institutions for customer authentication. Where these security applications were once on the analog side of things, today they are purely digital and connected to the Internet, acting as validation tools that communicate with customers’ wearables to authenticate them, completing the IoT cycle with minimum input from customers.

Perhaps one of the more popular aspects of IoT in Fintech lies in the retail industry, with tech giants taking up initiatives that offer customers a self-checkout service enabled by their IoT devices such as wearables, so they can avoid waiting in line at cashiers and just walk out of the store while having their cards scanned by devices upon their exit.

Another prominent application of IoT is when smart kitchen appliances replenish their missing components by themselves, as when for example a coffee filter needs to be changed, reminding the consumer to replace it but also ordering and paying for it without any input from anyone.

IoT can even enhance the physical operations inside a bank or similar traditional FI, meaning it’s not just an enabler of the digital world. Customers are reluctant to visit their bank’s branches today, but the implementation of smart systems inside the branch makes it much easier and time-saving, such as having IoT technology that offers navigation inside the bank for customers, or even matching them to the correct representative based on their request.

When comparing the rising popularity of IoT to FinTech in its infant stage, one could deduct that acceptance rates are somewhat similar, although FinTech was a much broader concept in the finance world. Banks and FIs were reluctant at some point to adapt FinTech products & services to their offerings, yet today FinTech is a major part of their strategic vision. In that regard, IoT is similar in that it’s obviously not just another buzzword, and it’s here to stay.

Market leaders are in the process of establishing partnerships with a wide selection of IoT companies, in anticipation of the inevitable future of connected things as facilitators of digital payments with minimal effort involved. Financial institutions should take note of their leading counterparts, mainly because huge non-finance organizations could end up taking the lead when it comes to IoT, and that would entail a much more competitive environment for FIs to relate to.

Financial institutions and IoT, as it was with FinTech, have a great advantage over emerging companies; trust and loyalty. Customers tend to hang on to their banks when satisfied, and these banks should tackle this when considering venturing into IoT. Their expertise and reliability in the market should act as a robust backbone for their already-loyal customers, so upon releasing an IoT initiative, product or service, their customers should flock effortlessly to their innovative solution; however banks need to be vigilant in ensuring that they deploy a platform that is worthy of their customers’ trust and loyalty, so that they retain those users and move forward with them into the future of the Internet of Things.

3

3

0

0

10.9k

10.9k

.jpg)

Comments